Which Of The Following Is The Correct Accounting Equation

News Leon

Apr 03, 2025 · 5 min read

Table of Contents

Which of the Following is the Correct Accounting Equation? A Deep Dive into the Fundamental Accounting Equation

The accounting equation is the bedrock of double-entry bookkeeping. Understanding it is crucial for anyone involved in finance, accounting, or business management. But with various formulations floating around, it's easy to get confused. This article will delve deep into the fundamental accounting equation, exploring its components, applications, and variations, ultimately answering the question: which of the following is the correct accounting equation? We'll clarify common misconceptions and provide practical examples to solidify your understanding.

Understanding the Fundamental Accounting Equation

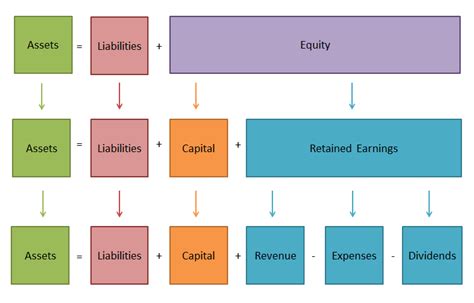

The fundamental accounting equation, also known as the balance sheet equation, expresses the relationship between a company's assets, liabilities, and equity. It states that:

Assets = Liabilities + Equity

This seemingly simple equation holds immense power. It reflects the fundamental principle that every transaction affects at least two accounts. Let's break down each component:

1. Assets

Assets represent a company's possessions and resources that have economic value and are expected to provide future benefits. These can be tangible, like:

- Current Assets: Assets expected to be converted into cash within one year, including cash, accounts receivable, inventory, and prepaid expenses.

- Non-Current Assets: Assets with a useful life exceeding one year, including property, plant, and equipment (PP&E), intangible assets (patents, copyrights), and long-term investments.

2. Liabilities

Liabilities represent a company's obligations to others. These are debts or financial obligations that the company must settle in the future. Examples include:

- Current Liabilities: Short-term debts due within one year, such as accounts payable, salaries payable, short-term loans, and taxes payable.

- Non-Current Liabilities: Long-term debts due beyond one year, including long-term loans, mortgages, bonds payable, and deferred revenue.

3. Equity

Equity, also known as net worth or shareholders' equity, represents the residual interest in the assets of an entity after deducting its liabilities. It's essentially the owners' stake in the company. For corporations, this includes:

- Common Stock: Represents the ownership shares issued to investors.

- Retained Earnings: Accumulated profits that haven't been distributed as dividends.

- Treasury Stock: Company's own stock that it has repurchased.

Why the Accounting Equation Always Balances

The accounting equation always balances because every transaction affects at least two accounts. For example:

- Purchasing Equipment with Cash: This increases the company's assets (equipment) and simultaneously decreases assets (cash). The overall equation remains balanced.

- Taking out a Loan: This increases assets (cash) and increases liabilities (loan payable). The equation remains balanced.

- Earning Revenue: This increases assets (cash or accounts receivable) and increases equity (retained earnings). Again, the equation remains balanced.

This balancing act is the cornerstone of double-entry bookkeeping, ensuring accuracy and preventing errors. Any imbalance indicates a mistake in recording the transaction.

Variations and Misconceptions

While the fundamental equation (Assets = Liabilities + Equity) is the most common, some variations exist, but they're essentially rearrangements of the same core principle. For instance:

- Assets - Liabilities = Equity: This shows equity as the difference between assets and liabilities.

- Assets - Equity = Liabilities: This highlights liabilities as the difference between assets and equity.

A common misconception is that the accounting equation only applies to corporations. This is incorrect. The equation is applicable to all types of business entities, including sole proprietorships, partnerships, and non-profit organizations. The only difference might lie in how equity is presented (e.g., owner's equity instead of shareholders' equity).

Practical Applications of the Accounting Equation

The accounting equation is more than just a theoretical concept; it has numerous practical applications:

- Balance Sheet Preparation: The equation forms the basis for constructing a company's balance sheet, a crucial financial statement showcasing the company's financial position at a specific point in time.

- Financial Statement Analysis: Analyzing the relationship between assets, liabilities, and equity reveals crucial insights into a company's financial health, liquidity, and solvency.

- Transaction Recording: Every business transaction is recorded using the accounting equation, ensuring that the double-entry system remains balanced.

- Fraud Detection: Any deviation from the accounting equation can be a red flag, signaling potential errors or fraudulent activities.

- Business Valuation: Understanding the components of the equation helps in valuing a business by assessing its assets, liabilities, and ultimately, its net worth (equity).

Answering the Question: Which Accounting Equation is Correct?

There isn't one "correct" accounting equation in the sense of multiple fundamentally different equations. The core principle remains consistent: Assets = Liabilities + Equity. Any other variation is simply a rearrangement of this fundamental equation, expressing the same relationship between the three core elements. Choosing the best representation often depends on the context and the information you want to emphasize. However, remembering and understanding the fundamental equation (Assets = Liabilities + Equity) is paramount.

Advanced Considerations: Understanding Equity in Detail

While the basic accounting equation provides a strong foundation, a deeper understanding of equity is crucial for more advanced accounting concepts. Equity is impacted by various factors beyond simply retained earnings. These include:

- Owner's Investments: Additional capital invested by the owners increases equity.

- Dividends Paid: Distributions of profits to shareholders decrease equity.

- Revenue and Expenses: Profits (revenue exceeding expenses) increase retained earnings and thus equity, while losses decrease it.

- Share Repurchases (Treasury Stock): Buying back company stock reduces equity.

- Stock Issuances: Issuing new shares increases equity.

Therefore, a more nuanced view of the accounting equation might involve showing the individual components of equity explicitly. However, even this level of detail doesn't change the fundamental relationship: assets always equal liabilities plus equity.

Conclusion: Mastering the Accounting Equation

The accounting equation is a fundamental concept in accounting and finance. Its simplicity belies its profound importance. By grasping its core components and variations, you gain a critical understanding of a company's financial health, the mechanics of double-entry bookkeeping, and the ability to analyze financial statements effectively. Remember, while variations exist, the underlying principle remains the same: Assets = Liabilities + Equity. This understanding will serve as a solid foundation for further exploration of accounting principles and financial analysis. Mastering this equation is a crucial step toward becoming financially literate.

Latest Posts

Latest Posts

-

Containing Two Different Alleles For A Trait

Apr 04, 2025

-

Which Of The Following Is A Non Renewable Source Of Energy

Apr 04, 2025

-

What Binds To The Exposed Cross Bridges On Actin

Apr 04, 2025

-

All Squares Are Rectangles And Rhombuses

Apr 04, 2025

-

What Is The Role Of Toothpaste In Preventing Cavities

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about Which Of The Following Is The Correct Accounting Equation . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.