The Typical Production Possibilities Curve Is

News Leon

Mar 15, 2025 · 6 min read

Table of Contents

The Typical Production Possibilities Curve: A Comprehensive Guide

The production possibilities curve (PPC), also known as the production possibility frontier (PPF), is a fundamental concept in economics illustrating the maximum possible output combinations of two goods or services an economy can achieve with its available resources and technology. Understanding the PPC is crucial for grasping core economic principles like scarcity, opportunity cost, efficiency, and economic growth. This comprehensive guide will delve into the intricacies of the typical PPC, exploring its assumptions, interpretations, and implications.

Understanding the Basics of the PPC

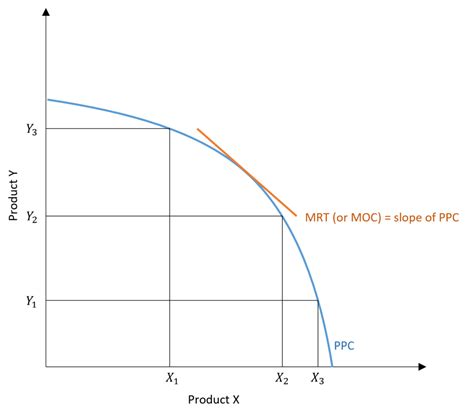

The PPC is typically represented graphically as a downward-sloping curve. Each point on the curve represents a combination of two goods that an economy can produce when utilizing all its resources efficiently. Any point inside the curve indicates inefficient resource allocation, while points outside the curve are unattainable with the current resources and technology.

Key Assumptions of the PPC:

- Fixed Resources: The model assumes a fixed quantity of resources (land, labor, capital, and entrepreneurship) available for production. This simplifies the analysis by focusing on the efficient allocation of existing resources.

- Fixed Technology: The technology used in production remains constant. Advances in technology would shift the PPC outward, representing increased potential output.

- Full Employment: All resources are fully employed; there is no unemployment of labor or underutilization of capital.

- Two Goods: The model typically simplifies the analysis by considering only two goods. This makes it easier to visualize the trade-offs involved. While the principle extends to multiple goods, the two-good model offers a clear introduction.

Interpreting the PPC:

The downward slope of the PPC illustrates the concept of opportunity cost. To produce more of one good, the economy must sacrifice some production of the other good. The slope of the curve at any point represents the marginal rate of transformation (MRT), which is the rate at which one good must be given up to produce an additional unit of the other good.

Points on the PPC:

- Points on the Curve: These points represent efficient production. All resources are fully utilized, and the economy is producing the maximum output possible given its resources and technology.

- Points Inside the Curve: These points represent inefficient production. Resources are underutilized, and the economy could produce more of both goods by using its resources more effectively. This might be due to unemployment, technological inefficiencies, or other factors.

- Points Outside the Curve: These points are unattainable with the current resources and technology. To reach these points, the economy would need to increase its resources, improve its technology, or both.

The Shape of the PPC: Linear vs. Concave

While often depicted as a concave curve, the PPC can also be linear, depending on the assumptions made about the resources and their suitability for producing different goods.

Linear PPC:

A linear PPC implies a constant opportunity cost. This occurs when resources are perfectly adaptable between the production of the two goods. For example, if producing both goods requires the same resources in the same proportions, then switching production between them would involve a constant trade-off.

Concave PPC:

A concave PPC, the more typical representation, implies an increasing opportunity cost. This is more realistic, as resources are not perfectly adaptable. Some resources are better suited to producing one good than the other. As the economy produces more of one good, it must increasingly sacrifice larger amounts of the other good because it is using resources that are less and less efficient at producing the second good. This is also referred to as the law of increasing opportunity cost.

Shifts in the PPC: Economic Growth

The PPC is not static; it can shift outward or inward depending on changes in the economy's capacity to produce goods and services. This shift is usually a result of economic growth.

Outward Shifts (Economic Growth):

An outward shift of the PPC indicates economic growth. This occurs when:

- Technological advancements: Improvements in technology allow for more efficient production, increasing the potential output of both goods.

- Increased resources: An increase in the quantity of resources (e.g., through population growth, discovery of new resources, or investment in capital goods) expands the economy's production possibilities.

- Improved human capital: Investments in education and training enhance the productivity of the labor force.

Inward Shifts (Economic Decline):

An inward shift of the PPC indicates economic decline. This can be due to:

- Natural disasters: Events like earthquakes or floods can destroy resources and reduce production capacity.

- Wars or conflicts: Conflicts can disrupt production and destroy resources.

- Resource depletion: Overexploitation of natural resources can lead to a decrease in production possibilities.

- Technological regression: A loss of technological knowledge can reduce the efficiency of production.

Applications of the PPC

The PPC is not just a theoretical model; it has practical applications in various economic contexts:

- Resource allocation decisions: Governments and businesses can use the PPC to analyze the trade-offs involved in allocating resources to different sectors of the economy. For instance, a government might use a PPC to analyze the trade-off between military spending and social programs.

- Economic policy evaluation: The PPC can be used to evaluate the impact of different economic policies on the economy's productive capacity. For example, analyzing the effect of trade liberalization on the overall output of an economy can be aided with a PPC.

- Long-term economic planning: The PPC provides a framework for long-term economic planning, helping policymakers to identify potential growth areas and allocate resources accordingly. It aids in making decisions about future investment in technology and human capital.

- International trade: The PPC can illustrate comparative advantage and the potential gains from trade between countries. Countries can specialize in producing goods they are relatively more efficient at producing and then trade with other countries for goods they are less efficient at producing, leading to higher overall output for both countries.

Limitations of the PPC

While the PPC is a valuable tool, it has limitations:

- Simplified model: The PPC is a simplified model that only considers two goods. In reality, economies produce thousands of goods and services.

- Constant technology assumption: The model assumes constant technology. In the real world, technological advancements constantly change the production possibilities.

- Fixed resources assumption: The assumption of fixed resources ignores the possibility of resource discovery or depletion.

Conclusion: A Powerful Tool for Economic Analysis

The production possibilities curve, despite its simplifying assumptions, remains a powerful tool for understanding fundamental economic principles. It effectively illustrates the concept of scarcity, opportunity cost, efficiency, and economic growth. By visualizing the trade-offs inherent in resource allocation, the PPC helps economists, policymakers, and businesses make informed decisions about resource allocation and economic development. Understanding its intricacies provides a solid foundation for more advanced economic analysis. The dynamic nature of the PPC, capable of shifting outward with growth and inward with decline, highlights the importance of innovation, investment, and sustainable resource management for long-term economic prosperity. Its applications extend across various economic contexts, making it an indispensable tool in the economist's toolkit.

Latest Posts

Latest Posts

-

Iodine Is Essential For The Synthesis Of

Mar 15, 2025

-

Is Osmosis High To Low Or Low To High

Mar 15, 2025

-

Concave Mirror And Convex Mirror Difference

Mar 15, 2025

-

Which Is Not A Cranial Bone Of The Skull

Mar 15, 2025

-

Mountain Range That Separates Europe And Asia

Mar 15, 2025

Related Post

Thank you for visiting our website which covers about The Typical Production Possibilities Curve Is . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.