Costs Which Do Not Change With The Level Of Output

News Leon

Apr 05, 2025 · 7 min read

Table of Contents

Costs Which Do Not Change With the Level of Output: A Comprehensive Guide to Fixed Costs

Understanding costs is crucial for any business, regardless of size or industry. A key element of cost accounting is differentiating between fixed and variable costs. This article delves deep into fixed costs, those expenses that remain constant regardless of the level of output or sales volume. We'll explore their nature, implications, examples, and how businesses manage them for optimal profitability.

What are Fixed Costs?

Fixed costs, also known as indirect costs or overhead costs, are expenses that don't fluctuate with changes in production or sales. They represent a consistent financial obligation for a business, irrespective of whether it produces one unit or a thousand. These costs are essential for the operation of the business but are not directly tied to the creation of goods or services.

Key characteristics of fixed costs:

- Constant over a specific period: Fixed costs remain relatively stable within a defined range of production. This period is usually a short-term accounting period, such as a month or a quarter. However, it’s crucial to note that these costs can change over the long term.

- Independent of output: The amount spent on fixed costs does not depend on the number of units produced or sold.

- Essential for business operation: These costs are necessary for the business to function, even if it's not producing anything.

Types of Fixed Costs

Fixed costs can be further categorized into several subtypes:

1. Committed Fixed Costs:

These are long-term expenses that are difficult to adjust in the short term, even if production levels change significantly. These costs often involve significant financial commitments and are typically associated with long-term contracts or investments.

Examples of Committed Fixed Costs:

- Depreciation: The systematic allocation of the cost of an asset over its useful life. This applies to buildings, machinery, and equipment. The depreciation expense is fixed regardless of production.

- Rent: Monthly or annual rent payments for office space, factory space, or retail locations are a classic example of a committed fixed cost. The rent remains the same whether the space is fully utilized or partially empty.

- Salaries of Permanent Staff: The salaries paid to permanent employees (excluding temporary or hourly workers) represent a significant committed fixed cost. These salaries are generally fixed regardless of production volume.

- Insurance Premiums: Insurance costs for property, liability, or workers' compensation are typically fixed for a policy period.

- Property Taxes: Annual property taxes on business real estate remain constant regardless of output.

2. Discretionary Fixed Costs:

Unlike committed fixed costs, discretionary fixed costs are more flexible and can be adjusted in the short term. These expenses are often associated with non-essential business activities but are still considered fixed because their expenditure isn't directly tied to production volume.

Examples of Discretionary Fixed Costs:

- Advertising and Marketing Expenses: While a company can adjust its advertising budget, the overall budget for a specific period remains fixed.

- Research and Development (R&D): A company may allocate a certain amount for R&D annually, regardless of production.

- Training and Development: Costs associated with employee training programs are typically fixed for a given period.

- Membership Fees (professional organizations): These are usually fixed annual fees.

- Donations and Sponsorships: Charitable contributions and sponsorships are examples of discretionary fixed costs.

The Importance of Understanding Fixed Costs

Understanding fixed costs is critical for several reasons:

- Profitability Analysis: Knowing your fixed costs is vital for calculating your break-even point—the level of production where total revenue equals total costs. This information helps determine pricing strategies and production targets.

- Cost Control: Identifying and managing fixed costs is crucial for cost control and increasing profitability. By carefully analyzing discretionary fixed costs, businesses can find areas for potential savings.

- Decision Making: Accurate fixed cost data is essential for making informed decisions about investments, expansion plans, and other strategic initiatives.

- Financial Planning and Forecasting: Accurate fixed cost data allows for better financial planning, forecasting, and budgeting.

Fixed Costs vs. Variable Costs

It’s crucial to distinguish fixed costs from variable costs, which change directly with the level of production. Variable costs include direct materials, direct labor, and some utilities.

| Feature | Fixed Costs | Variable Costs |

|---|---|---|

| Definition | Costs that remain constant regardless of output | Costs that change directly with output |

| Relationship to Output | Independent of output | Directly proportional to output |

| Examples | Rent, salaries, depreciation, insurance | Raw materials, direct labor, packaging |

| Short-term Flexibility | Less flexible | More flexible |

How Businesses Manage Fixed Costs

Businesses employ various strategies to manage and control their fixed costs:

- Negotiating better terms: Businesses can negotiate lower rent, insurance premiums, or other fixed costs by leveraging their bargaining power.

- Optimizing resource utilization: Improving efficiency in resource utilization can help reduce fixed costs associated with utilities, equipment maintenance, and administrative overheads.

- Outsourcing: Outsourcing certain functions can reduce fixed costs associated with salaries, office space, and equipment.

- Automation: Automating certain processes can lead to long-term savings in labor and other variable costs, potentially offsetting some fixed costs associated with the automation investment.

- Right-sizing: If a business experiences a sustained decline in production or sales, it may need to downsize to reduce fixed costs such as salaries and rent. This often involves difficult but necessary decisions.

- Strategic planning: Long-term strategic planning plays a crucial role in managing fixed costs. This includes carefully considering factors like location, facility size, and investment in technology before committing to significant fixed costs.

The Impact of Fixed Costs on Pricing and Profitability

Fixed costs significantly impact pricing strategies and overall profitability. A high proportion of fixed costs can mean that a business needs to sell a higher volume of goods or services to break even. Conversely, a lower proportion of fixed costs allows for greater profitability at lower sales volumes.

Businesses with high fixed costs are often more sensitive to fluctuations in demand. During periods of low demand, they may struggle to cover their fixed costs, while businesses with lower fixed costs are better positioned to weather such periods.

Long-Term Implications of Fixed Costs

While fixed costs remain constant in the short term, they can change over the long run. This is particularly true for committed fixed costs, such as rent or property taxes. Businesses must consider the long-term implications of fixed costs when making investment decisions. Changes in technology, market conditions, and business strategy can all affect the level of fixed costs over time. Regular reviews and adjustments are crucial to ensure long-term financial health and stability.

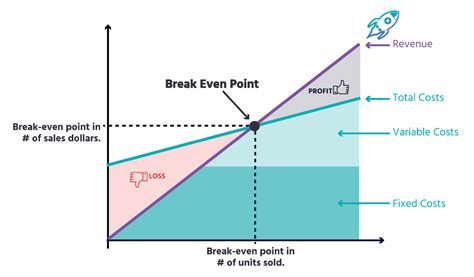

Fixed Costs and Break-Even Analysis

Understanding fixed costs is paramount in break-even analysis. The break-even point is the level of sales at which total revenue equals total costs (fixed costs plus variable costs). This critical point helps businesses determine the minimum sales volume necessary to avoid losses.

The formula for calculating the break-even point in units is:

Break-even point (units) = Fixed Costs / (Selling Price per Unit - Variable Cost per Unit)

By understanding their fixed costs, businesses can accurately determine their break-even point and adjust pricing or production accordingly to achieve profitability.

Conclusion: Strategic Management of Fixed Costs is Key

Fixed costs are an unavoidable part of running a business. However, by understanding their nature, types, and impact on profitability, businesses can develop strategies to effectively manage and control them. Strategic planning, cost optimization, and regular review are crucial for maximizing profitability and ensuring long-term success. A comprehensive grasp of fixed costs empowers businesses to make informed decisions, navigate market fluctuations, and achieve sustainable growth. Ignoring fixed costs can lead to financial instability, while effectively managing them can significantly enhance a company's bottom line. Therefore, continuous monitoring and strategic adaptation regarding fixed costs are vital aspects of effective business management.

Latest Posts

Latest Posts

-

Which Ratio Is Equivalent To 2 5

Apr 05, 2025

-

What Is The Lcm Of 6 And 20

Apr 05, 2025

-

Diff Between Cell Wall And Cell Membrane

Apr 05, 2025

-

Which Of The Following Is The Major Site Of Photosynthesis

Apr 05, 2025

-

The Pigment Molecules Responsible For Photosynthesis Are Located In The

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about Costs Which Do Not Change With The Level Of Output . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.