An Account Will Have A Credit Balance If The

News Leon

Apr 05, 2025 · 7 min read

Table of Contents

An Account Will Have a Credit Balance If… Understanding Debits and Credits

Understanding debits and credits is fundamental to accounting. While seemingly simple, the concept can be confusing for beginners. This comprehensive guide will delve deep into the circumstances that lead to a credit balance in an account, clarifying the nuances and providing practical examples. We will explore various account types and explain how debits and credits impact their balances. By the end, you’ll have a solid grasp of credit balances and how they fit into the broader accounting framework.

What are Debits and Credits?

Before diving into credit balances, let's solidify our understanding of debits and credits. These are simply bookkeeping entries that record financial transactions. They represent increases or decreases in account balances depending on the type of account.

The fundamental accounting equation provides the framework:

Assets = Liabilities + Equity

This equation must always balance. Any transaction affecting one side of the equation must also affect the other to maintain equilibrium. Debits and credits are the mechanisms that ensure this balance.

The Rules:

The rules governing debits and credits are simple but crucial:

-

For Assets, Expenses, and Dividends: A debit increases the balance, and a credit decreases the balance. Think of "debit" as adding to these accounts.

-

For Liabilities, Equity, and Revenue: A credit increases the balance, and a debit decreases the balance. "Credit" adds to these accounts.

This seemingly simple set of rules is the bedrock of double-entry bookkeeping. Every transaction affects at least two accounts, ensuring the accounting equation remains balanced.

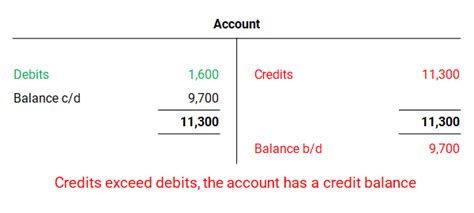

When Does an Account Have a Credit Balance?

An account will have a credit balance when the total of its credit entries exceeds the total of its debit entries. This occurs predominantly in accounts that naturally hold credit balances:

1. Liability Accounts:

Liability accounts represent obligations a business owes to others. These include:

-

Accounts Payable: Money owed to suppliers for goods or services purchased on credit. A credit increases this account (increasing the amount owed), and a debit decreases it (reducing the amount owed). Naturally, this account typically shows a credit balance.

-

Notes Payable: Formal written promises to repay borrowed money. Similar to accounts payable, a credit increases the amount owed, and a debit reduces it. A credit balance is expected.

-

Salaries Payable: Wages owed to employees but not yet paid. A credit increases the amount owed, and a debit decreases it. This account normally has a credit balance.

-

Unearned Revenue: Payments received for goods or services that haven't yet been delivered or performed. A credit increases this account (representing the revenue yet to be earned), and a debit decreases it (as services are rendered or goods delivered). A credit balance is typical here.

-

Bonds Payable: Money borrowed through the issuance of bonds. A credit increases the borrowed amount, while a debit represents repayment or repurchase. A credit balance is standard.

Example: Imagine a company receives $10,000 for a service to be delivered in the future. This increases Unearned Revenue with a credit of $10,000. As the service is delivered, the Unearned Revenue is decreased with a debit, and Revenue is increased with a credit to reflect the earned income.

2. Equity Accounts:

Equity accounts represent the owners' stake in the business. These include:

-

Capital Stock: The amount invested by shareholders in a corporation. A credit increases the capital stock (reflecting additional investment), while a debit reduces it (e.g., repurchasing shares). Typically shows a credit balance.

-

Retained Earnings: Accumulated profits of a company that haven't been distributed as dividends. A credit increases retained earnings (reflecting profits), and a debit decreases it (reflecting losses or dividend payments). Usually carries a credit balance (unless the company has accumulated net losses).

-

Revenue Accounts: Represent increases in a company's net worth due to the sale of goods or services. Credits increase revenue, while debits decrease it (e.g., to correct errors). These accounts usually show a credit balance, representing increases in net worth.

Example: A company makes a sale for $5,000. This increases Revenue with a credit of $5,000. This credit increases the retained earnings, ultimately increasing equity and maintaining the balance sheet equation.

3. Credit Balances in Unusual Circumstances:

While less common, a credit balance can appear in accounts that usually hold debit balances due to errors or specific transactions.

-

Accounts Receivable: Typically a debit balance (money owed to the company), a credit balance could indicate a credit memo issued to a customer to correct an overpayment or error.

-

Cash: While normally showing a debit balance, a credit balance could result from accounting errors or an unexpected bank overdraft that’s not immediately reconciled.

-

Inventory: A credit balance might signify an error in recording inventory adjustments or returns.

It's crucial to investigate any unexpected credit balances in debit-oriented accounts immediately to identify and correct the underlying errors.

Analyzing Credit Balances:

Understanding why an account holds a credit balance is vital for accurate financial reporting and decision-making. A credit balance signifies a different financial position compared to a debit balance. For instance:

-

A credit balance in Accounts Payable suggests that the company owes money to its suppliers. This needs to be managed carefully to maintain healthy supplier relationships and avoid late payment penalties.

-

A credit balance in Retained Earnings implies accumulated profits. This indicates the financial health of the business and allows for reinvestment, dividend payments, or debt reduction.

-

An unexpected credit balance in a typically debit account highlights an accounting error requiring investigation and correction. Failure to address this could lead to misrepresentation of the company’s financial status.

Debits and Credits in Practice: Illustrative Examples

Let's illustrate the concepts with some examples:

Example 1: Accounts Payable

A company purchases $2,000 worth of supplies on credit. The journal entry would be:

| Account | Debit | Credit |

|---|---|---|

| Supplies | $2,000 | |

| Accounts Payable | $2,000 |

This increases the Supplies account (a debit increase for assets) and increases Accounts Payable (a credit increase for liabilities), maintaining the accounting equation. Accounts Payable now shows a credit balance of $2,000.

Example 2: Sales Revenue

A company makes a sale of $10,000 in cash. The journal entry would be:

| Account | Debit | Credit |

|---|---|---|

| Cash | $10,000 | |

| Sales Revenue | $10,000 |

This increases the Cash account (a debit increase for assets) and increases Sales Revenue (a credit increase for revenue), keeping the equation balanced. Sales Revenue displays a credit balance of $10,000.

Example 3: Retained Earnings

The company from Example 2 had net income of $5,000 for the period. This is closed to retained earnings at the end of the accounting period:

| Account | Debit | Credit |

|---|---|---|

| Income Summary | $5,000 | |

| Retained Earnings | $5,000 |

Income summary is a temporary account used to close revenue and expenses at the end of the period. This entry increases retained earnings (a credit increase for equity) with the net income. This further increases the credit balance in retained earnings.

Conclusion: Mastering Debits and Credits

Understanding debits and credits, and consequently, the situations that lead to credit balances, is fundamental to accurate financial record-keeping. While the rules might seem initially complex, consistent practice and a clear grasp of the accounting equation will build confidence. Remember, every transaction impacts at least two accounts, always maintaining the essential balance. By consistently applying the debit and credit rules, and carefully analyzing account balances, businesses can ensure accurate financial reporting, informed decision-making, and a healthy financial position. Regularly reviewing and reconciling accounts will also help detect and correct any errors that might lead to unusual or unexpected balances. The key is practice and a commitment to understanding the underlying principles.

Latest Posts

Latest Posts

-

Which Ratio Is Equivalent To 2 5

Apr 05, 2025

-

What Is The Lcm Of 6 And 20

Apr 05, 2025

-

Diff Between Cell Wall And Cell Membrane

Apr 05, 2025

-

Which Of The Following Is The Major Site Of Photosynthesis

Apr 05, 2025

-

The Pigment Molecules Responsible For Photosynthesis Are Located In The

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about An Account Will Have A Credit Balance If The . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.