Managerial Accounting Information Is Generally Prepared For

News Leon

Mar 20, 2025 · 6 min read

Table of Contents

Managerial Accounting Information: Who Uses It and Why?

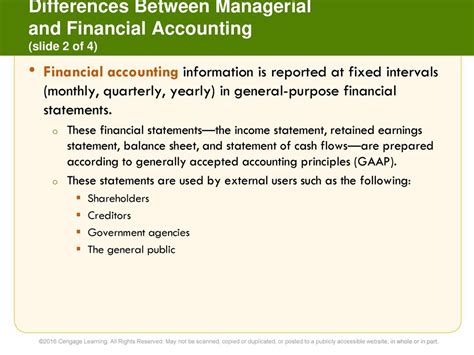

Managerial accounting, unlike financial accounting, doesn't produce reports for external stakeholders like investors or creditors. Instead, its focus is entirely internal. This article delves deep into the various users of managerial accounting information and the specific reasons why this information is crucial for their decision-making processes. We'll explore the diverse applications, demonstrating the multifaceted nature of managerial accounting and its indispensable role in organizational success.

Key Users of Managerial Accounting Information

The primary users of managerial accounting information are internal to the organization. This includes a wide range of individuals and departments, each with their own unique needs and information requirements. Let's examine these key user groups in detail:

1. Management (Executives, Managers, Supervisors)

Management at all levels relies heavily on managerial accounting data to make informed strategic and operational decisions. This information is vital for:

-

Strategic Planning: Long-term strategic plans rely on accurate forecasts of sales, costs, and profits. Managerial accounting provides the data needed to assess market opportunities, develop new products or services, and expand into new markets. Detailed cost analysis, for instance, is crucial for determining pricing strategies and evaluating the potential profitability of new ventures.

-

Operational Control: Day-to-day operations require constant monitoring and adjustments. Managerial accounting systems provide real-time data on production efficiency, inventory levels, sales performance, and other key metrics. This allows managers to identify bottlenecks, improve processes, and ensure that resources are utilized effectively. Variance analysis, comparing actual results to budgeted figures, is a critical tool in operational control.

-

Performance Evaluation: Managerial accounting data is essential for evaluating the performance of individuals, departments, and the organization as a whole. Key Performance Indicators (KPIs), such as return on investment (ROI), net present value (NPV), and customer satisfaction ratings, are regularly tracked and analyzed to identify areas for improvement and reward successful performance.

-

Decision-Making: From minor operational choices to major capital investments, managerial accounting information informs every decision a manager makes. Cost-benefit analysis, break-even analysis, and other decision-making tools rely on the accurate and timely data provided by managerial accounting systems.

2. Department Heads and Supervisors

Department heads and supervisors use managerial accounting information to:

-

Monitor departmental performance: They use data to track departmental efficiency, productivity, and adherence to budgets. This allows them to identify and address areas of weakness and celebrate successes within their teams.

-

Allocate resources effectively: Based on performance data and projected needs, department heads determine how best to allocate personnel, equipment, and other resources to maximize efficiency and output.

-

Improve departmental processes: By analyzing cost data and production statistics, supervisors can pinpoint bottlenecks, inefficiencies, and areas for improvement within their departments.

-

Manage budgets: Supervisors are responsible for creating and managing departmental budgets, which requires detailed forecasting and monitoring of expenses and revenues. Managerial accounting provides the tools and data to make accurate budget projections and track performance against the budget.

3. Product Managers

Product managers utilize managerial accounting data for:

-

Product costing: Accurate product costing is crucial for pricing decisions, determining profitability, and making decisions about product life cycles. This involves allocating both direct and indirect costs to individual products.

-

Product line profitability analysis: Analyzing the profitability of individual product lines allows product managers to identify which products are contributing most to overall profitability and which ones require attention or may need to be discontinued.

-

New product development: Managerial accounting data informs decisions about the feasibility of developing new products. This includes cost estimations, market analysis, and projected profitability.

-

Pricing strategies: Understanding product costs and market conditions allows product managers to set optimal pricing strategies to maximize profitability.

4. Marketing and Sales Teams

Marketing and sales teams rely on managerial accounting information for:

-

Marketing campaign effectiveness: Tracking marketing expenses and sales revenue allows marketers to measure the effectiveness of various campaigns and allocate resources more effectively.

-

Sales forecasting: Sales forecasts, based on historical data and market trends, are crucial for planning production, inventory levels, and resource allocation.

-

Pricing analysis: Managerial accounting information helps in determining optimal pricing strategies, taking into account cost structure, competitor pricing, and market demand.

-

Customer profitability analysis: Identifying and focusing on high-value customers is essential for maximizing profitability. Managerial accounting helps segment customers based on profitability.

5. Production and Operations Teams

Production and operations teams use managerial accounting data for:

-

Production planning and scheduling: Accurate cost information, production capacity, and demand forecasts are vital for effective production planning.

-

Inventory management: Monitoring inventory levels, costs, and turnover rates helps optimize inventory management and reduce waste.

-

Quality control: Managerial accounting can be used to track quality control metrics and identify areas for improvement in the production process.

-

Process improvement: Analyzing production costs and efficiency allows operations teams to identify bottlenecks and implement process improvements.

Types of Managerial Accounting Information Used

The information provided by managerial accounting is diverse and tailored to the specific needs of each user. Some common types of information include:

-

Cost Accounting Data: This includes data on direct and indirect costs, manufacturing overhead, and product costs. This information is crucial for pricing decisions, profitability analysis, and cost control.

-

Budgetary Information: Budgets are crucial for planning and control. They provide a framework for comparing actual results to planned performance and identifying variances.

-

Performance Reports: These reports compare actual performance to planned performance, highlighting areas of success and areas needing improvement. They typically include key performance indicators (KPIs) such as return on investment (ROI), profit margins, and productivity metrics.

-

Sales Data: This includes information on sales volume, revenue, sales trends, and customer segmentation.

-

Inventory Data: This includes data on inventory levels, costs, turnover rates, and obsolescence.

-

Production Data: This includes information on production volume, efficiency, quality control, and waste.

-

Financial Statements (Internal): While financial accounting focuses on external reporting, managerial accounting uses internal financial statements (often more detailed) for internal analysis and decision-making.

The Importance of Timely and Accurate Information

The usefulness of managerial accounting information is directly tied to its timeliness and accuracy. Outdated or inaccurate information can lead to poor decisions, wasted resources, and missed opportunities. Therefore, robust systems for data collection, processing, and analysis are essential. These systems must be designed to provide information quickly and accurately, allowing for timely interventions and course corrections. Regular audits and reviews of the managerial accounting system ensure continued accuracy and reliability.

Conclusion: Managerial Accounting – The Engine of Internal Decision-Making

Managerial accounting information is not just data; it's the lifeblood of effective internal decision-making within an organization. From strategic planning to operational control, every aspect of business operations relies on the insights provided by a well-designed and implemented managerial accounting system. Understanding the various users of this information, the types of data they require, and the importance of timeliness and accuracy is critical for organizations seeking to optimize performance, enhance profitability, and achieve their strategic goals. By harnessing the power of managerial accounting, organizations can navigate the complexities of the business world with confidence and achieve sustainable success.

Latest Posts

Latest Posts

-

Which Of The Following Is The Correct Equation For Photosynthesis

Mar 20, 2025

-

Which Three Dimensional Figure Has Exactly Three Rectangular Faces

Mar 20, 2025

-

What Is The Difference Between Milligrams And Milliliters

Mar 20, 2025

-

Metals Are Good Conductors Of Electricity

Mar 20, 2025

-

In Which Layer Of The Atmosphere Does Most Weather Occur

Mar 20, 2025

Related Post

Thank you for visiting our website which covers about Managerial Accounting Information Is Generally Prepared For . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.