Increasing Marginal Opportunity Cost Implies That

News Leon

Apr 05, 2025 · 6 min read

Table of Contents

Increasing Marginal Opportunity Cost Implies That... Diminishing Returns

The concept of increasing marginal opportunity cost is fundamental to economics, particularly in understanding production possibilities frontiers (PPFs) and resource allocation. It's a crucial element in demonstrating why economic decisions are rarely simple and often involve trade-offs. This article will delve deep into this principle, explaining what it means, why it occurs, and its implications for various economic scenarios.

Understanding Opportunity Cost

Before diving into increasing marginal opportunity cost, let's establish a clear understanding of opportunity cost itself. Opportunity cost represents the value of the next best alternative forgone when making a choice. It's essentially the cost of not choosing the other option. For instance, if you choose to spend an hour studying economics, the opportunity cost is the value of what you could have done with that hour—perhaps watching a movie, exercising, or working on a side hustle.

The key takeaway here is that opportunity cost is subjective. Its value differs from person to person based on individual preferences and circumstances. What one person considers a valuable use of their time, another might deem less important.

Marginal Opportunity Cost: A Step Further

Marginal opportunity cost focuses on the additional opportunity cost incurred when increasing the production or consumption of a good or service by one unit. It represents the slope of the production possibility frontier (PPF) at a specific point. This slope indicates the rate at which society must give up the production of one good to produce an additional unit of another.

Imagine a farmer who can produce either wheat or corn. Initially, shifting resources from wheat to corn production might only require a small reduction in wheat output. However, as more resources are allocated to corn production, the farmer may need to sacrifice increasing amounts of wheat to produce each additional unit of corn. This is where the concept of increasing marginal opportunity cost comes into play.

Increasing Marginal Opportunity Cost: The Core Principle

Increasing marginal opportunity cost implies that the more of a good or service we produce, the greater the opportunity cost of producing an additional unit. This is because resources are not perfectly adaptable to all types of production. Some resources are better suited for producing certain goods than others. As we try to produce more of a particular good, we're forced to use resources that are less efficient at producing that good, leading to a higher opportunity cost.

Think of it like this: A baker can use her oven to bake either bread or cakes. Initially, shifting some oven time from bread to cakes might be easily absorbed without significantly reducing bread production. However, as she dedicates more and more oven time to cakes, the decrease in bread production becomes proportionally larger. This is because she's starting to use her oven time less efficiently for bread production, thus incurring a higher opportunity cost.

Why Does Increasing Marginal Opportunity Cost Occur?

Several factors contribute to the phenomenon of increasing marginal opportunity cost:

-

Resource Specialization: Resources are not equally versatile. Some resources are better suited for producing certain goods than others. As production of a specific good increases, we're forced to use less efficient resources, leading to a higher opportunity cost.

-

Diminishing Returns: As more and more resources are allocated to the production of a single good, the marginal product of those resources eventually begins to decline. This means that each additional unit of resource added to production yields smaller and smaller increases in output. This diminishing return makes it increasingly expensive to produce additional units.

-

Different Resource Qualities: Even within the same category of resource, there are quality differences. For example, some land is more fertile than others. As we produce more of a good that requires land, we may need to use less fertile land, leading to a higher opportunity cost.

-

Imperfect Substitutability: Resources are not perfectly interchangeable. We can't always substitute one resource for another without incurring some cost or efficiency loss. This lack of perfect substitutability leads to increasing opportunity costs as we shift resources from one type of production to another.

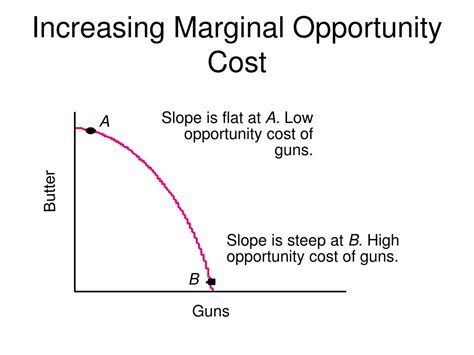

Graphical Representation: The PPF

The production possibility frontier (PPF) is a graphical tool used to illustrate the concept of opportunity cost and its relationship to resource scarcity. The PPF shows the maximum possible combinations of two goods that an economy can produce with its available resources and technology.

A bowed-out PPF, which is the most common representation, visually depicts increasing marginal opportunity cost. The steeper slope of the PPF at higher levels of one good's production indicates a higher opportunity cost of producing an additional unit.

Implications of Increasing Marginal Opportunity Cost

The principle of increasing marginal opportunity cost has profound implications across various economic domains:

-

Resource Allocation: Understanding increasing marginal opportunity cost is crucial for efficient resource allocation. Economists and policymakers use this principle to make informed decisions about which goods and services to prioritize, given the scarcity of resources.

-

Economic Growth: Economic growth involves expanding the PPF outward. This expansion can occur through technological advancements, increases in the quantity of resources, or improvements in resource efficiency. By addressing the factors that contribute to increasing marginal opportunity cost, economies can enhance their production possibilities and achieve higher levels of economic growth.

-

Trade-offs and Decision-Making: The reality of increasing marginal opportunity cost emphasizes that economic choices involve trade-offs. There is no such thing as a free lunch. Every decision entails forgoing alternative opportunities. Understanding this principle empowers individuals and businesses to make more informed and efficient choices.

-

Comparative Advantage and International Trade: The concept of comparative advantage, which states that nations should specialize in producing and exporting goods in which they have a lower opportunity cost, is directly linked to increasing marginal opportunity cost. By specializing, countries can take advantage of their comparative advantage and achieve greater overall economic output through trade.

-

Public Policy: Government policies, such as taxes, subsidies, and regulations, can influence the opportunity cost of different activities. By carefully considering the implications of increasing marginal opportunity cost, policymakers can design more effective policies that promote economic efficiency and social welfare.

Increasing Marginal Opportunity Cost and Efficiency

The increasing marginal opportunity cost curve highlights the trade-offs inherent in resource allocation. Efficient allocation occurs where the marginal benefit from producing one more unit of a good is equal to the marginal cost, which includes the opportunity cost. However, as opportunity costs increase, achieving this efficient allocation becomes more challenging.

Exceptions and Considerations

While increasing marginal opportunity cost is a general rule, there might be exceptions in specific situations. For instance, with constant returns to scale in production, a linear PPF might be observed. However, these instances are typically limited and often represent simplified models rather than accurately representing the complexities of real-world production processes.

Conclusion

Increasing marginal opportunity cost is a fundamental economic principle that underscores the scarcity of resources and the importance of making efficient choices. It explains why the production of additional units of a good becomes increasingly expensive in terms of the opportunity cost of forgoing the production of other goods. This principle permeates all aspects of economic activity, from individual consumption decisions to national resource allocation strategies. By understanding and applying this principle, we can achieve more efficient resource utilization, foster economic growth, and make more informed decisions in various economic contexts. Understanding increasing marginal opportunity cost is essential for comprehending the complexities of economic decision-making and resource allocation in a world characterized by scarcity. Its implications are far-reaching, influencing everything from personal choices to global trade patterns.

Latest Posts

Latest Posts

-

What Is The Formula For The Compound Iron Iii Sulfate

Apr 06, 2025

-

Using Osmotic Pressure To Find Molar Mass

Apr 06, 2025

-

Oxidation Number Of O In Oh

Apr 06, 2025

-

Use The Following Phrases In Your Own Sentences

Apr 06, 2025

-

How Many Chromosomes Will Be In Each Daughter Cell

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about Increasing Marginal Opportunity Cost Implies That . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.