Which Of The Following Is True Of Annuities

News Leon

Apr 06, 2025 · 6 min read

Table of Contents

Which of the following is true of annuities? Demystifying Retirement Income Options

Annuities are a powerful financial tool, but also a complex one, often shrouded in mystery and misconception. Understanding their nuances is crucial for anyone planning for retirement. This comprehensive guide will delve into the characteristics of annuities, helping you separate fact from fiction and determine which statements about annuities are truly accurate. We'll explore different types of annuities, their benefits, drawbacks, and crucial considerations before investing.

Before we dissect common statements about annuities, let's establish a foundational understanding. An annuity is a financial product that provides a stream of payments over time. These payments can be for a specified period or for the lifetime of the annuitant (the person receiving the payments). They are often used as a retirement income strategy to supplement Social Security and other retirement savings.

Now, let's address some common statements about annuities and determine their truthfulness.

Common Statements About Annuities: Fact or Fiction?

Here are some frequently encountered statements regarding annuities, analyzed for accuracy:

1. "Annuities guarantee a stream of income for life."

Truth: Partially True. This depends entirely on the type of annuity. Fixed annuities generally guarantee a minimum rate of return and a fixed stream of payments for a specified period or for life. However, the purchasing power of that fixed income may erode due to inflation. Variable annuities, on the other hand, offer no such guarantee. The income stream fluctuates based on the performance of the underlying investments. While they might offer potentially higher returns, there's also a risk of losing principal. Indexed annuities offer a blend of these, providing a minimum guaranteed return while allowing potential growth linked to a market index. The guarantee is typically tied to the initial invested amount.

2. "Annuities are always a good investment."

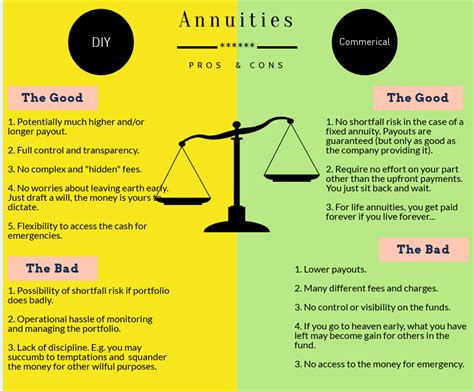

Truth: False. Annuities are not a one-size-fits-all solution. They are complex financial products with fees and surrender charges that can significantly impact returns. Whether an annuity is a "good" investment depends heavily on your individual circumstances, risk tolerance, financial goals, and the specific annuity contract. It's crucial to carefully consider fees, surrender charges, and the potential for lower returns compared to other investment options. An annuity should be part of a diversified portfolio strategy, not your sole retirement plan.

3. "Annuities are only for retirees."

Truth: False. While annuities are frequently used by retirees to generate income, they can also serve other purposes. Some individuals use annuities to:

- Accumulate wealth: Deferred annuities allow you to invest money tax-deferred, growing your investment before accessing it during retirement.

- Protect against longevity risk: Annuities can provide lifelong income, helping to prevent outliving your savings.

- Leave a legacy: Some annuities offer death benefits, allowing you to pass on a portion of your investment to heirs.

4. "All annuities are the same."

Truth: False. There is a wide variety of annuity types, each with its own set of features, benefits, and risks. Key distinctions include:

- Fixed vs. Variable: As mentioned previously, fixed annuities offer a guaranteed return, while variable annuities offer potentially higher returns but carry investment risk.

- Immediate vs. Deferred: Immediate annuities begin paying out immediately after purchase, while deferred annuities offer tax-deferred growth until payments begin.

- Single Premium vs. Periodic Premium: Single premium annuities are purchased with a lump sum, while periodic premium annuities allow for regular contributions.

- Indexed Annuities: These combine elements of fixed and variable annuities, offering potential market-linked growth with a guaranteed minimum return.

5. "Annuities are heavily regulated, protecting investors."

Truth: Partially True. Annuities are regulated at the state level, and generally, these regulations aim to protect consumers from fraud and misrepresentation. However, the complexity of annuity contracts and the potential for high fees can still pose challenges for investors. It's crucial to understand the terms and conditions of any annuity before investing and to seek professional advice. Do not solely rely on the regulatory framework.

Understanding Annuity Types in Detail

Let's explore the most common types of annuities in greater detail to further solidify our understanding:

1. Fixed Annuities:

- Guaranteed Return: These offer a fixed interest rate for a specified period, guaranteeing a steady stream of income. This predictability makes them attractive to risk-averse individuals.

- Low Growth Potential: The fixed interest rate often lags behind inflation, potentially eroding purchasing power over time.

- Suitable For: Individuals seeking a low-risk, stable income stream and prioritizing security over growth.

2. Variable Annuities:

- Investment Choices: These invest in various sub-accounts, allowing for potential growth but also carrying investment risk. The returns are not guaranteed.

- Higher Growth Potential: If the investments perform well, these annuities can provide significantly higher returns than fixed annuities.

- Risk of Loss: There's a risk of losing principal if the underlying investments underperform.

- Suitable For: More risk-tolerant investors seeking potentially higher returns but willing to accept market fluctuations.

3. Indexed Annuities:

- Combination of Fixed and Variable: These offer a minimum guaranteed return while allowing for potential growth based on the performance of a market index (e.g., the S&P 500).

- Participation Rates: They typically don't provide 100% participation in the index's gains. A participation rate determines the percentage of the index's growth credited to the annuity.

- Crediting Strategies: Different crediting strategies exist, affecting how index performance translates into annuity growth.

- Suitable For: Individuals seeking a balance between growth potential and risk mitigation.

4. Immediate Annuities:

- Immediate Income: These begin paying out immediately after purchase. The payments can be for a fixed period or for life.

- No Growth Period: There's no accumulation period, as the money is immediately used to generate income.

- Suitable For: Individuals requiring an immediate stream of income, often in retirement.

5. Deferred Annuities:

- Tax-Deferred Growth: These accumulate funds tax-deferred until payments begin. This allows for growth without paying taxes on the earnings until withdrawal.

- Flexibility: These annuities allow for flexibility in the timing of payments.

- Suitable For: Individuals aiming to accumulate wealth over time and defer taxes.

Crucial Considerations Before Investing in an Annuity

Before you invest in an annuity, carefully consider the following factors:

- Fees and Charges: Annuities often carry significant fees, including mortality and expense risk charges, surrender charges (penalties for early withdrawal), and administrative fees. These fees can significantly impact your overall returns. Thoroughly review the annuity contract's fee schedule.

- Tax Implications: While annuities offer tax-deferred growth, withdrawals are subject to income tax. Understand the tax implications of your chosen annuity before investing. Consult a tax professional.

- Liquidity: Annuities are not typically highly liquid. Early withdrawals may incur significant surrender charges. Consider your need for access to your funds before investing.

- Your Financial Goals: Annuities are best used as part of a larger retirement strategy that aligns with your individual financial objectives and risk tolerance. Avoid using annuities as your sole retirement solution.

- Professional Advice: Seeking guidance from a qualified financial advisor is crucial before making any annuity investment decision. An advisor can help you evaluate your needs and determine whether an annuity is appropriate for you.

Conclusion: Annuities – A Powerful Tool, But Use with Caution

Annuities can be a valuable component of a comprehensive retirement plan, offering the potential for guaranteed income and tax advantages. However, they are complex financial products with potential downsides. It's essential to understand the various types of annuities, their associated fees, and the inherent risks involved before investing. Thorough research, careful consideration, and professional guidance are crucial for making informed decisions that align with your financial goals and risk tolerance. Remember, no single statement can encompass the multifaceted nature of annuities; a thorough understanding of individual contract terms is paramount. Always seek advice from a qualified professional before making any investment decisions.

Latest Posts

Latest Posts

-

Why Are Cellular Respiration And Photosynthesis Opposite Processes

Apr 09, 2025

-

Name 2 Parts Of The Stamen

Apr 09, 2025

-

Which Is The Largest Sense Organ

Apr 09, 2025

-

Where Does Glycolysis Occur In Eukaryotic Cells

Apr 09, 2025

-

Contain Carbon Hydrogen Oxygen And Nitrogen

Apr 09, 2025

Related Post

Thank you for visiting our website which covers about Which Of The Following Is True Of Annuities . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.