What Are The Determinants Of Supply

News Leon

Mar 17, 2025 · 6 min read

Table of Contents

What Are the Determinants of Supply? A Comprehensive Guide

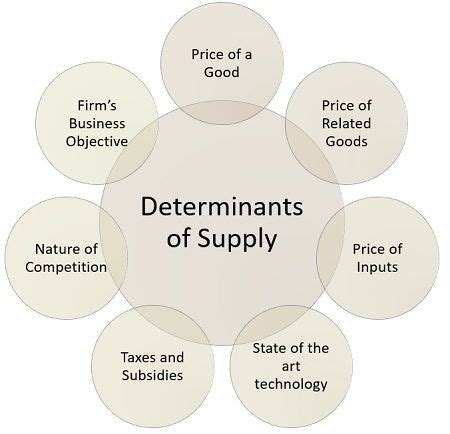

Understanding the determinants of supply is crucial for anyone involved in economics, business, or market analysis. Supply, simply put, represents the amount of a good or service that producers are willing and able to offer at a given price. However, this willingness and ability are influenced by a multitude of factors, extending far beyond just the price itself. This article will delve deep into these determinants, providing a comprehensive overview for a thorough understanding of the dynamics of supply.

The Price of the Good or Service Itself

The most fundamental determinant of supply is, of course, the price of the good or service. This forms the bedrock of the law of supply: all other factors being equal (ceteris paribus), as the price of a good increases, the quantity supplied will increase, and vice versa. This inverse relationship is depicted by the upward-sloping supply curve. Producers are incentivized to supply more at higher prices because they can earn greater profits. Conversely, at lower prices, the profitability decreases, potentially leading to reduced production or even exiting the market.

However, it's crucial to remember the ceteris paribus clause. This condition emphasizes that this relationship holds true only if other factors remain constant. A change in any of these other factors will shift the entire supply curve, rather than simply moving along it.

Costs of Production

A significant influence on a producer's willingness to supply is the cost of production. This encompasses all expenses involved in producing a good or service, including:

1. Raw Materials:

Fluctuations in the prices of raw materials directly impact the cost of production. If the price of a key raw material increases, the cost of producing the final good rises, leading to a decrease in supply at any given price. For example, a rise in the price of cotton will directly impact the supply of cotton shirts.

2. Labor Costs:

Labor costs, including wages, benefits, and training expenses, are a major component of production costs. Increases in minimum wage or union negotiations leading to higher wages can increase the cost of production, thereby decreasing supply. Technological advancements that substitute labor with capital can, conversely, reduce costs and increase supply.

3. Capital Costs:

Capital costs encompass expenses related to machinery, equipment, and technology. The cost of acquiring and maintaining these assets can significantly influence the cost of production. Investments in new technology can potentially decrease production costs in the long run, leading to increased supply. Conversely, higher interest rates making borrowing more expensive can reduce investments and decrease supply.

4. Energy Costs:

The cost of energy—whether electricity, fuel, or other energy sources—is a critical determinant, especially for energy-intensive industries. Rising energy prices directly translate to higher production costs and thus a decrease in supply.

Technology

Technological advancements play a pivotal role in shaping supply. Innovations that improve production efficiency, reduce waste, or automate processes can dramatically lower costs and increase the quantity supplied at each price. This leads to a rightward shift in the supply curve. For example, the introduction of automated assembly lines in car manufacturing increased the supply of vehicles significantly.

Conversely, a lack of technological progress or reliance on outdated methods can lead to higher costs and decreased supply.

Government Policies

Government intervention through various policies can significantly impact supply. These policies include:

1. Taxes:

Taxes on production, such as excise taxes or sales taxes, increase the cost of production, thus reducing the quantity supplied. Higher taxes can discourage production, especially for goods with relatively inelastic demand.

2. Subsidies:

Subsidies, on the other hand, are government payments that reduce the cost of production. Subsidies incentivize producers to increase supply by making the production process more profitable. Agricultural subsidies are a common example of this.

3. Regulations:

Regulations, such as environmental regulations or labor laws, can impact supply. While some regulations might increase costs (e.g., stricter environmental standards), others may improve efficiency or safety, potentially leading to long-term improvements in supply. The net effect depends on the specific regulation and its impact on production costs.

4. Trade Policies:

Trade policies, including tariffs and quotas, significantly affect supply. Tariffs (taxes on imported goods) can reduce the supply of imported goods within a country, while quotas (limits on imported quantities) directly restrict supply. Conversely, free trade agreements can increase supply by allowing access to cheaper imports or larger export markets.

Producer Expectations

Producer expectations regarding future prices play a substantial role in current supply decisions. If producers anticipate future price increases, they may choose to withhold some of their current supply, hoping to sell it at a higher price later. This leads to a decrease in current supply. Conversely, expectations of price declines may lead producers to increase their current supply to avoid losses.

Number of Sellers

The number of sellers (or firms) in a market directly affects the overall supply. An increase in the number of firms competing in a market increases the total quantity supplied at any given price, resulting in a rightward shift of the market supply curve. Conversely, a decrease in the number of firms due to mergers, bankruptcies, or exit from the market will decrease the total quantity supplied.

Input Prices of Other Goods

The prices of inputs used to produce other goods can also indirectly affect supply. If a firm uses the same resources to produce multiple goods, a rise in the price of one good may incentivize the firm to allocate more resources to that good, thereby reducing the supply of the other goods. For example, if the price of wheat increases significantly, farmers might shift their resources towards wheat cultivation, thus potentially decreasing the supply of other crops.

Natural Events and Disasters

Natural events and disasters, such as hurricanes, floods, earthquakes, or droughts, can drastically impact supply. These events can disrupt production, destroy infrastructure, damage crops, or limit access to resources, leading to a significant decrease in supply. The effects can be short-term or long-term, depending on the severity of the event and the industry's resilience.

The Role of Time

The impact of the determinants of supply can vary significantly depending on the time horizon. In the short run, many factors are fixed, such as the size of the factory or the amount of installed capital. Changes in price primarily affect the quantity supplied along a given supply curve. In the long run, however, firms have more flexibility to adjust their production capacity, leading to greater responsiveness to price changes and changes in other determinants of supply.

Conclusion: A Dynamic Interplay

The determinants of supply are intricately interconnected, and their impact is rarely isolated. A change in one factor often triggers ripple effects across others. For example, rising energy prices (a cost of production) may lead producers to invest in more energy-efficient technologies (technological advancements), potentially mitigating the initial negative impact on supply in the long run.

Understanding this dynamic interplay is crucial for accurate market forecasting and informed business decision-making. By considering all the determinants of supply, economists and business professionals can gain a more complete picture of market behavior and develop more effective strategies. This knowledge is essential for navigating the complexities of the market, managing risks, and maximizing opportunities.

Latest Posts

Latest Posts

-

Lines Of Symmetry On A Trapezoid

Mar 18, 2025

-

Two Same Words With Different Meanings

Mar 18, 2025

-

Select The Correct Statement About Equilibrium

Mar 18, 2025

-

Draw The Major Product Of The Following Reaction

Mar 18, 2025

-

A Wire Loop Of Radius 10 Cm And Resistance

Mar 18, 2025

Related Post

Thank you for visiting our website which covers about What Are The Determinants Of Supply . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.